Bitcoin Magazine

No – Digital Credit Cannot Be Replicated With Bitcoin and Treasuries

The scale up of STRC and SATA has drawn in many detractors.

Recently Onramp published a paper highlighting some issues of Digital Credit. There were some errors and the paper was clearly AI-generated in most places. My favorite error actually had little to do with Digital Credit, and it appeared in the preface of the report (imagine you haven’t even started reading the actual paper and you already see a factual error, this is the level of AI we are dealing with).

Onramp writes on Page 3: “Strategy has released AI-generated advertising featuring a young, attractive model in a tropical setting”

But a quick viewing of the 30-second ad they are referencing shows that the woman worked “hard as an engineer”, not a model. This is literally 10 seconds into the ad, which is about the same amount of time it took me to spot the error in Onramp’s preface.

I just thought this anecdote was funny. Onto my main point.

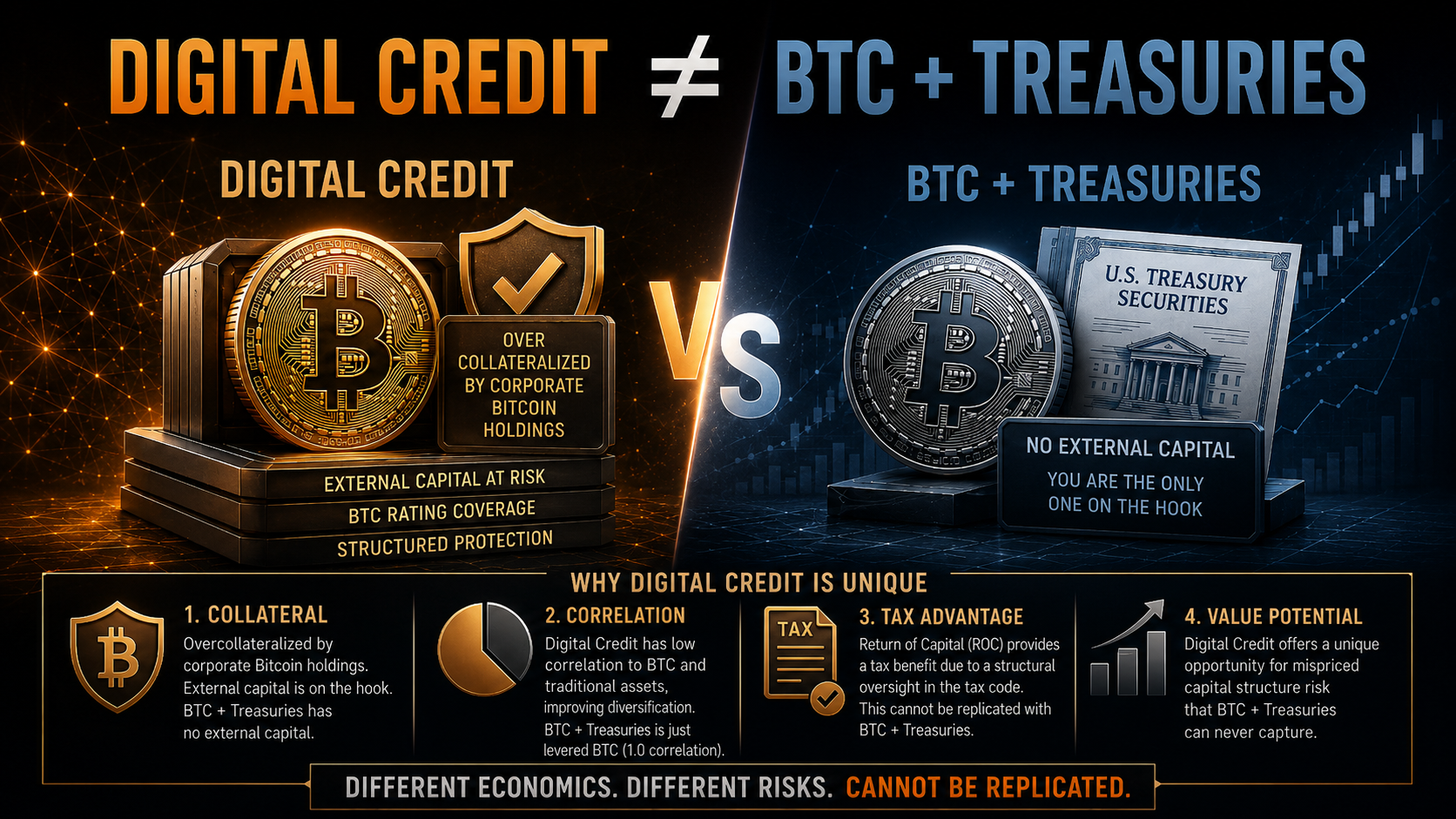

Their core argument was that Digital Credit could be better replicated by combining U.S. treasury securities with BTC. (This is what Onramp calls “the simpler trade” but I also fail to see how this is simpler considering that buying digital credit involves just one single ticker while “the simpler trade” involves a dynamic re-laddering of maturing treasury bonds combined with BTC held on a separate venue.)

This conclusion is wrong. It is trivial to show that it is wrong empirically (one just has to look at the daily returns time series of Digital Credit instruments vs a portfolio of IBIT and SGOV or IEF). But this missive will present multiple economic arguments for why we can know a priori that the claim is incorrect.

Reason 1: Collateral

Digital Credit is overcollateralized by corporate bitcoin holdings. This cannot be replicated with one’s own equity because there is no committed external capital in the case of owning BTC and treasuries—it is all your own money and no one else is on the hook. Credit is different. Even though the principal is yours, there is external capital in the form of the issuer’s assets that are committed to ensuring you are made whole. This capital is “external” because it existed before you ever put your principal in and it remains well after you sell your position.

To be precise, an unencumbered bitcoin balance sheet isn’t collateral in the strict sense, but it serves as collateral in a flexible sense. For instance, a BTC-backed loan with margin call is collateralized in a strict sense because the collateral is set apart for the debt. Digital Credit gives the issuer more flexibility with collateral management, but it also gives the investor more flexibility because the security is fungible and liquid. This is an understanding that both parties agree to.

The presence of the collateral is protection for the investor. This coverage is expressed in the BTC